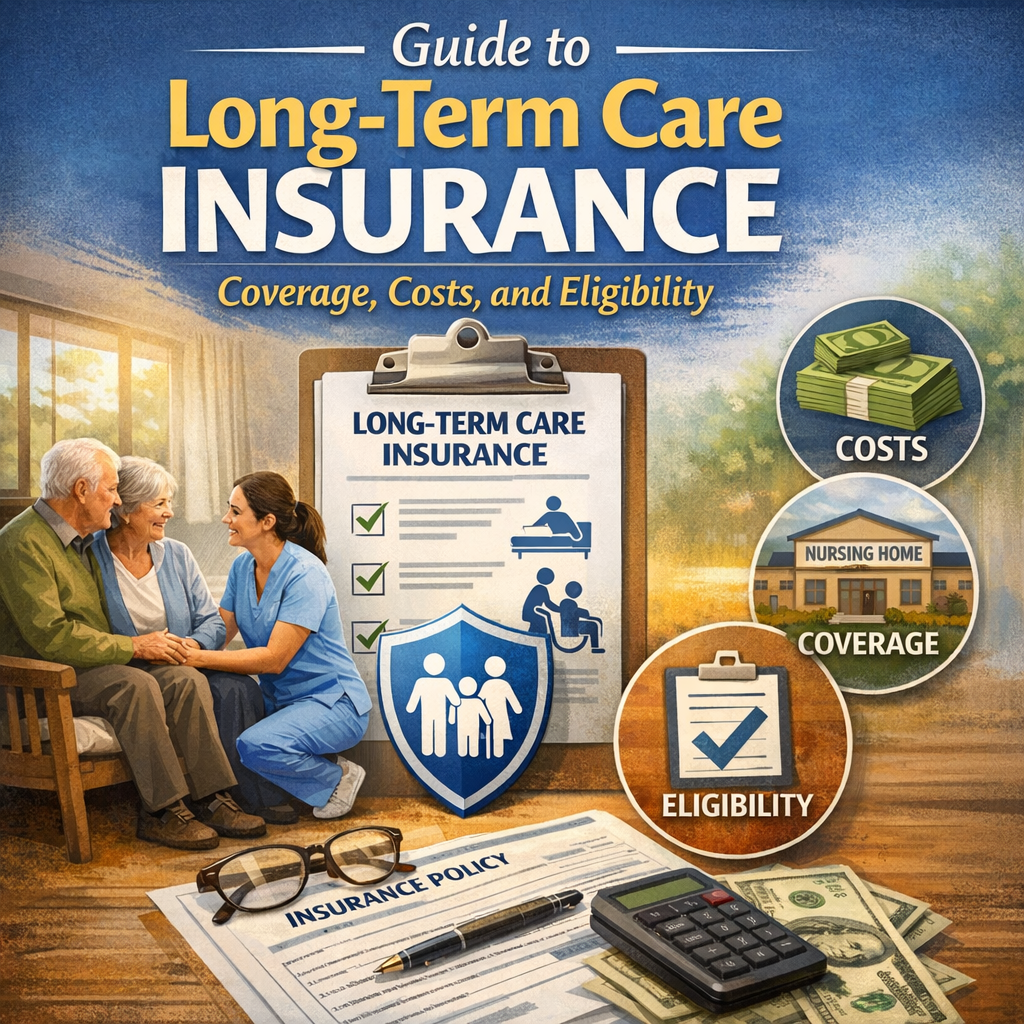

Guide to Long-Term Care Insurance: Coverage, Costs, and Eligibility

Understanding Long-Term Care Insurance: Coverage, Costs, and Eligibility

Long-term care insurance is an essential consideration for anyone planning for their future health needs. This type of insurance helps cover the cost of care not typically covered by regular health insurance, Medicare, or Medicaid. Understanding the coverage options, associated costs, and eligibility requirements can help individuals make informed decisions for their long-term health care planning.

What is Long-Term Care Insurance?

Long-term care insurance is designed to cover services and support needed by individuals who are unable to perform basic activities of daily living (ADLs) such as dressing, bathing, or eating. Coverage can include the cost of care provided at home, in the community, in assisted living facilities, or in nursing homes.

Coverage Options

Home Care

- In-Home Health Care: Services may include nursing care, physical therapy, or help with personal care from trained aides.

- Homemaker Services: Assistance with housekeeping, cooking, and shopping.

Community Services

- Adult Day Care Centers: These provide social and therapeutic services for adults who need supervision during the day.

- Respite Care: Temporary care to relieve family caregivers.

Facility Care

- Assisted Living Facilities (ALFs): For those who need help with ADLs but wish to live somewhat independently.

- Nursing Homes: Provide more comprehensive care for individuals with severe health conditions or cognitive impairments.

Costs of Long-Term Care Insurance

The costs of long-term care insurance vary widely based on several factors:

- Age at Purchase: Generally, premiums are lower when you purchase at a younger age.

- Health Status: Medical underwriting can affect costs; those in better health may receive lower premiums.

- Benefit Amount and Duration: The daily or monthly benefit amount and the length of time benefits are paid impact the premium.

- Inflation Protection: Riders that protect against inflation might increase costs but provide more comprehensive coverage over time.

Average Costs

According to recent data, the average annual premium for a 55-year-old couple was approximately $3,050. This illustrates the significant investment involved in securing long-term care insurance, but it also underscores its necessity given the high cost of long-term care services.

Eligibility for Coverage

Eligibility for long-term care insurance typically depends on the applicant’s health history and age. Insurers may require:

- Medical Screening: Most companies conduct health screenings or look through medical records.

- Age Limits: Some policies may not be available to new applicants over a certain age, often 75 or 80.

Who Should Consider Long-Term Care Insurance?

- Individuals Over 50: It’s often recommended to start looking at long-term care insurance options as you approach retirement age.

- Those with a Family History of Chronic Conditions: If chronic or debilitating conditions are common in your family history, considering long-term care insurance might be wise.

- People Without an Immediate Family Support System: Individuals without close family to rely on should consider long-term care insurance to ensure they have access to needed care.

Key Takeaways

Long-term care insurance is a significant part of planning for your health and financial future. It can alleviate financial pressure on family members and ensure you receive the care you need. Understanding the coverage options, the associated costs, and eligibility will help you choose the right plan for your circumstances. Always consult with a trusted insurance provider to explore your options thoroughly.

By investing in long-term care insurance, you’re not just planning for your future health needs; you’re also ensuring peace of mind for yourself and your loved ones. Being proactive now can save a lot of distress and financial difficulty later in life.